Systemic Risk Scorecard

July 9, 2026 — Systemic risk originates in the financial system—though it could be broader—with the possibility of adversely impacting the real economy. Agentic AI is the perfect tool for

July 9, 2026 — Systemic risk originates in the financial system—though it could be broader—with the possibility of adversely impacting the real economy. Agentic AI is the perfect tool for

July 3, 2026 — From our vantage point, the most interesting shift in market price action in June was the strong outperformance of value stocks compared to the broad market

June 5, 2026 — In the first few days of June, we are seeing a bit of a consolidation in markets after a blistering two-month run in all things tech

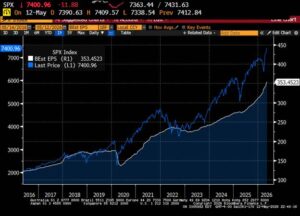

May 14, 2026 — It’s likely not a bubble. Earnings are high. Prices are high because they anticipate future high earnings growth. The historical record shows that growth rate is

May 3, 2026 — April saw a strong rally, which fully reversed the stock market’s losses in March. US markets set new all-time highs, and European stocks came within whispering

April 5, 2026 — March 2026 was a rough month for financial markets. Broad indexes experienced large selloffs, led by international stocks, though many of these still remain up in

March 21, 2026 — With apologies if this is the tenth investment piece you’ve read this week about the impact of the Iran War on asset markets, but we wanted

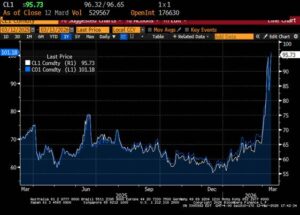

March 13, 2026 — Iran’s de facto closing of the Strait of Hormuz precipitated the latest in a series of energy crises. Since the 1970s, some energy spikes were associated

March 1, 2026 — AI fatigue has taken hold of financial markets. The companies powering the AI revolution (Nvidia, Google, Microsoft) were down. The companies that are being (or might