May 2025 Update

May 1, 2025 – While the S&P 500 index was almost unchanged in April, the dollar remained extremely weak, ending the month down over 4%. Since the beginning of February

May 1, 2025 – While the S&P 500 index was almost unchanged in April, the dollar remained extremely weak, ending the month down over 4%. Since the beginning of February

4/20/2025 — We wrote last year that gold typically does well when the Fed begins a monetary easing cycle. Since that time, the Fed has cut its interest rate target

4/4/2025 — To go along with my LinkedIn post on this topic, here are close-ups of the charts from Google Trends. And here is a figure from Shiller’s paper:

April 2, 2025 – To summarize the market action of March of 2025 in one chart: U.S. stocks (SPX) did poorly, international stocks (especially Europe, VGK) did well in dollar

March 18, 2025 — In a recent piece, we analyzed the construction of downside protected strategies. Here we propose a measure of the relative attractiveness of these strategies over time

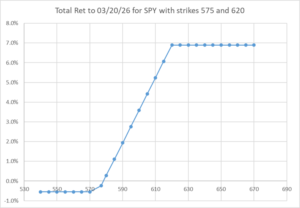

March 4, 2025 — Recently, downside protected ETFs have garnered a lot of investor attention. These products are long the stock market—via different indexes—and use options to create downside-protected payoffs.

March 2, 2025 – We wrote in last month’s letter that the U.S. stock market had to meet lofty earnings expectations to maintain its strong performance relative to global benchmarks,

February 2, 2025 — The DeepSeek blip notwithstanding (our initial take on the news is here), January 2025 was a good month for financial markets. The S&P 500 was up

January 18, 2025 — In his recent FT piece “How ‘the mother of all bubbles’ will pop,” Ruchir Sharma lays out the case for why U.S. stock market outperformance relative