February 3, 2023 —

Overview

One month into 2023, we take a pause to reflect on the major investing themes of 2022 and assess how these might play out in 2023. The dominant market theme of 2022 was the onset of global inflation and the subsequent central bank responses.

Some argue that central banks were behind the curve in addressing building inflationary pressures, but roughly a year of policy tightening has shown that global central banks were less behind the curve than is sometimes alleged.

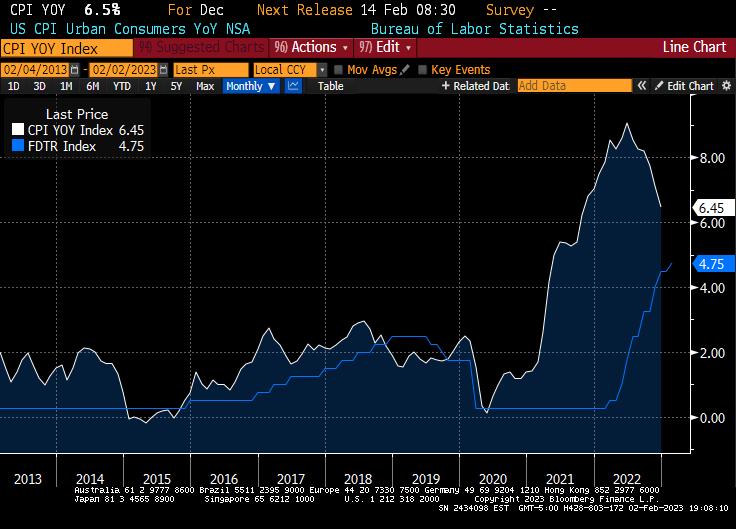

Inflation has started to come down, especially in the U.S., and markets have started to revise down their expectations for how much policy tightening will ultimately be needed. Federal Reserve Chair Jay Powell even uttered the word “disinflation” multiple times in his February 1st press conference following the Fed’s policy decision to hike the federal funds target rate by 25 basis points.

CPI year-over-year inflation and the Fed funds target rate (FDTR). Source: Bloomberg

Fears of a coordinated, global recession have also started to abate. Just recently, even the International Monetary Fund, an institution not prone to bouts of exuberance, revised upwards its global growth forecast relative to what it was predicting in October of 2022. Despite expectations to the contrary, Europe managed to eke out positive growth in Q4 2022. Even putting aside that recessions aren’t as terrible for stocks as the media would have you believe — as we’ve argued in the past — it no longer looks like a global recession is in the offing.

The paths of inflation and central bank monetary policy now look considerably more benign relative to the expectations of only a few weeks ago, and a global recession looks less likely.

The other big story that came, and somewhat went, in 2022 was the energy and commodity price spikes. The fears of an energy crunch on the back of Russia cutting off gas supplies to Europe and the more recent price caps imposed on Russian oil exports have also subsided (at least for the time being). Offsetting factors were a mild winter in Europe and the U.S., and good old-fashioned ingenuity, like the Germans quickly constructing LNG terminals to import non-Russian gas. As we’ve written in the past, global oil market supply appears tight, and a spike in demand, on top of the need to replenish U.S. Strategic Petroleum Reserves, may well lead to another sharp uptick in the energy complex. Energy (and commodity) prices have done nothing but go down since their early 2022 peak, but risks seem tilted to the upside in 2023.

The S&P Goldman Sachs Commodity Index and the front-month Brent future (CO1). Source: Bloomberg

Contributing to renewed hopes for brighter economic days in 2023 is the reopening of China, after three years of a zero-COVID policy, which ultimately strained social cohesion to the point that the government finally blinked in the early days of 2023. It appears that the majority of the Chinese population has already had COVID, suggesting that the reopening dynamic is poised to continue to play itself out over the coming weeks and months. Chinese stocks have been almost crypto-like in their rally from the lows of 2022. The Hong Kong focused FXI exchange traded fund is up over 50% from its lows of October 2022. If China growth really accelerates, which is the emerging consensus, this will provide yet another tailwind to the energy and commodity complex in 2023.

The combination of a less restrictive path of central bank policy and a China reopening surely bodes well for risk assets. And none of this has been lost on investors. This year’s extremely strong stock market performance across the globe bears witness to this fact. One month is surely not enough to undo all the negativity that was heaped onto financial markets in 2022, so the rally in risk assets may continue well into the new year.

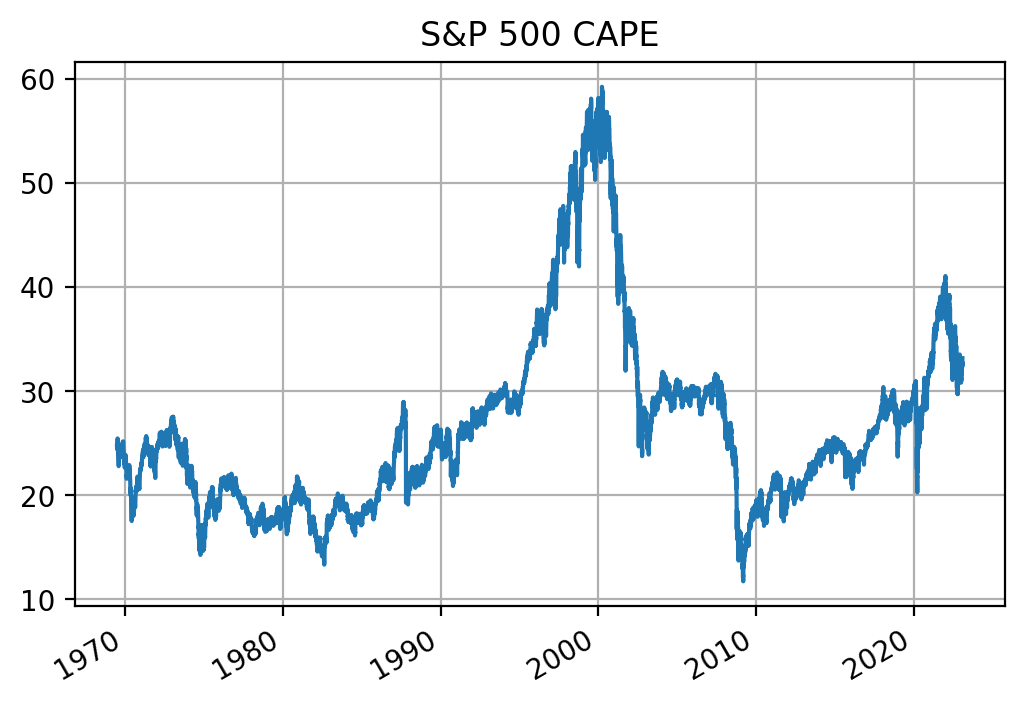

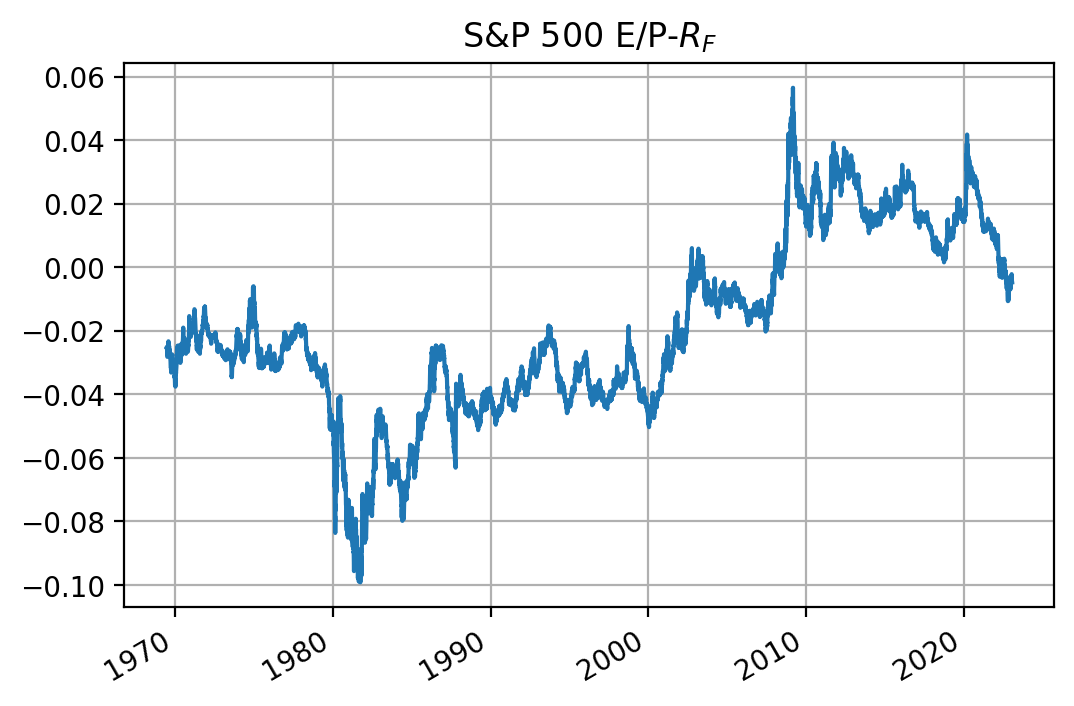

Cyclically-adjusted price to earnings ratio and excess earnings yield (E/P ratio minus the 10-year Treasury yield) for the S&P 500. Source: QuantStreet, Bloomberg

On a more cautionary note, valuations for the S&P 500 don’t seem particularly attractive, judging by either cyclically adjusted price-to-earnings ratios or earnings yields relative to 10-year Treasury rates. But two things are worth noting. First, valuation ratios haven’t had much to say about returns over the last decade. Second, high valuation ratios may well just be forecasting high earnings growth. If economic growth surprises on the upside, earnings growth can more than compensate for apparently elevated valuation ratios.

It should also be noted that several really nasty tail risks continue to lurk in the background. The tragedy going on in Ukraine does not appear to be abating. Risks of escalation remain and are very scary. Perhaps even more scary is the threat of a Taiwan-China conflict. One hopes and prays that sanity prevails and such things do not come to pass, but some smart people think this is a possibility. For the time being, these remain tail risks, but ones that bear close watching.

QuantStreet’s Positioning

How are we positioned in this investing landscape? As always, our approach is to be acutely aware of all the goings on in the world, but to also let the models speak. This combined quantamental approach leaves our portfolio as follows:

- In the core strategy, we are taking on a risk-level slightly higher than our risk benchmark. This reflects our view that, on balance, the current investing environment is attractive.

- We retain some non-U.S. exposure through foreign stock and government bond ETFs.

- Close to 90% of our exposure is in U.S. domestic assets which reflects the opinions of two distinct sets of models: both point to the U.S. being relatively more attractive than foreign investments.

- A chunk of our U.S. equity allocation is to value stocks, which (for the time being) look attractive on our valuation models relative to growth stocks.

- We also have exposure to real estate investment trusts, again on the back of that sector looking attractive in our valuation framework.

- Finally, for the reasons discussed, and because it remains the best performing asset over the prior year, we maintain an exposure to commodities via an ETF that tracks the S&P Goldman Sachs Commodity Index.

As always, our relative positioning in these asset classes reflects the portfolio with the highest expected return subject to our targeted risk level.

We are carefully watching market, geopolitical, and economic developments. As soon as conditions warrant, we are ready to react on our clients’ behalf.