May 3, 2026 —

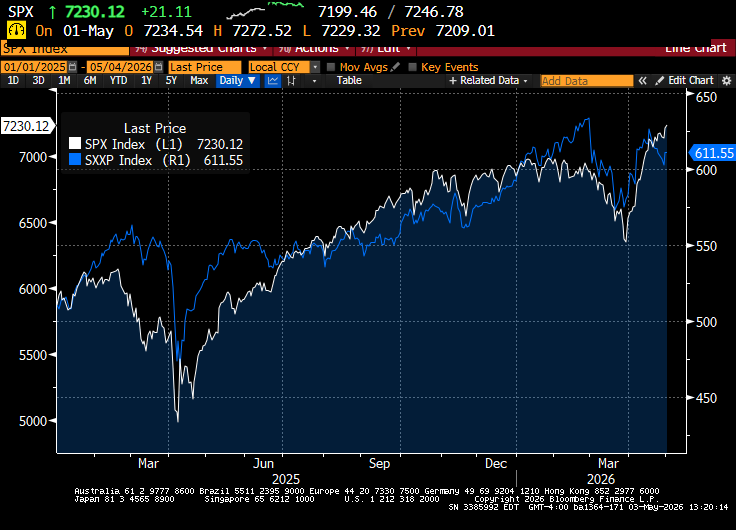

April saw a strong rally, which fully reversed the stock market’s losses in March. US markets set new all-time highs, and European stocks came within whispering distance of their all-time highs as well. This is the second time in two years that markets had a precipitous sell-off on the back of extremely bearish economic forecasts (first about the impact of tariffs and now about the oil price shock) which ultimately proved unfounded.

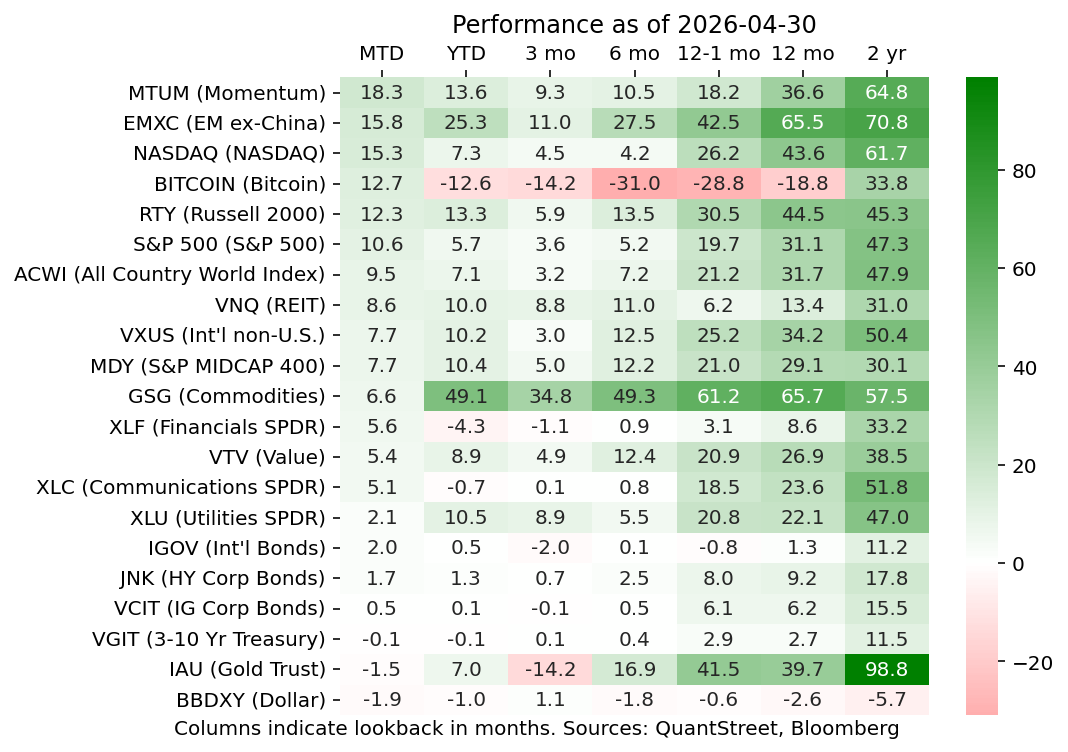

Looking across sectors, the strongest gains in April were in technology stocks, bitcoin, and smallcaps. EM ex-China, with its heavy exposure to Korean and Taiwanese stocks, was a stellar performer, reflecting the exposure of those countries’ economies to the AI semiconductor trade. The dollar largely reversed its March gains, and gold had another weak month. We’ve had gold in the portfolio for some time now, and are sticking with the exposure, largely on the back of our gradual de-dollarization thesis (see here for our reasons). For the time being, gold moves opposite to oil, as the market anticipates oil price increases will push back the timing of Fed interest rate cuts. These interest rate cuts are seen as positive for gold.

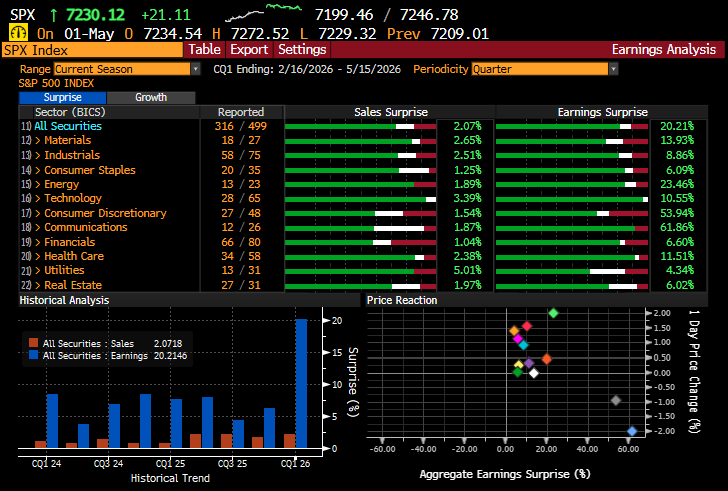

Not surprisingly, the large rally in stocks has coincided with an extremely strong earnings season. The table below, taken from Bloomberg, summarizes sales and earnings surprises by sector. With 316 of the S&P 500 companies reporting so far, the average sales beat (relative to analyst forecasts) is 2% and the average earnings beat is a whopping 20%. The bar chart at the bottom left of the page shows that both numbers are extremely high relative to past earnings seasons. Across sectors, the AI theme is pervasive. The two sectors with the strongest sales beats are technology and, especially, utilities as electrical grid capacity becomes a binding constraint in the AI buildout.

Part of what’s happening is that AI is slowly, or perhaps quickly, transitioning from economic potential to economic reality. We make three observations:

First, AI is starting to increase productivity. Stanford’s Erik Brynjolfsson estimates that productivity growth in the US—usually measured as real output per hour worked—nearly doubled in 2025 to 2.7% from its 1.4% growth rate over the prior decade. He writes that “[w]e are transitioning from an era of AI experimentation to one of structural utility.” As AI transitions into its utility phases, the ability to charge for AI services will grow rapidly.

Second, our own experience at QuantStreet confirms Brynjolfsson’s point. We went from using AI simply as a summarization tool—a capability we still use extensively in our investment process—to using AI to shape and drive our firm’s processes. In this context, we are using AI more and more. And AI is becoming pricier and pricier. We very frequently hit our daily and weekly usage limits for Claude, and then kick into overage rates. We are on the cusp of having to upgrade our Claude license to a higher use plan. Don’t tell Anthropic, but our willingness to pay is far higher than what they currently charge. But, to wit, I think the tech platforms already know this to be true.

Finally, an interesting thing is happening with AI and jobs. Apollo’s Torsten Slok refers to this as the Jevons’ paradox. See his Daily Spark piece from April 28, 2026. As AI makes some professional services, like consulting and business analysis, cheaper, the demand for these services grows, as do entry level jobs (those that are most susceptible to productivity gains from AI). Slok documents evidence of exactly this type of growth in the labor market. So not only is AI making firms more efficient, it is also (at least in some sectors) generating increased hiring. As we’ve argued before, this makes for a compelling investment backdrop.

Positioning for the month ahead

When constructing our monthly portfolios, we use estimates of asset class volatility and correlations calculated over the prior year. Last year’s market tariff tantrum started in March and really hit in April, and this left a trail of high volatility for the next year. The next chart shows a measure of the S&P 500 volatility calculated over the prior year. This measure peaked at 20 around the summer of last year, and slowly trended down. Finally, as April 2025 fell out of the sample, the volatility number dropped precipitously to the 12.5 level as of May of 2026. Our targeted portfolio volatilities—remember we construct portfolios to match the prior 12 month realized volatility of different stock/bond combinations, like 70/30, 80/20, and so on—all fell. Such a dramatic drop in volatility caused slight reallocations across our portfolios to achieve our respective risk targets. The most notable shifts were a few percentage point reallocation from stock into bond positions across most of our portfolios, except the highest risk ones.

Following the dramatic market rally of April and still simmering tensions in the Middle East, this bit of model-led tactical reallocations makes sense to us. We also added a small position in the materials sector (using the XLB ETF) across most of our portfolios. As always, the main driver was our systematic asset allocation process, a combination of our forecasting models coupled with a constrained portfolio optimizer. Qualitatively, our view is that the AI buildout will drive significant demand for many natural resources, like copper, steel, industrial gasses, and construction aggregates, which will generate positive operating fundamentals for the firms in XLB.

Working with QuantStreet

QuantStreet offers financial planning, wealth management, model portfolios, portfolio analytics, and a platform for advisors looking to gain independence. The firm’s investment approach is systematic, data-driven, and shaped by years of investing experience. To work with or learn more about QuantStreet, join our mailing list or contact us at hello@quantstreetcapital.com. Also, please sign up for our Substack.

QuantStreet is a registered investment advisor. Registration does not imply a certain level of skill or training. All financial forecasts are fraught with risk and uncertainty. Our views may prove incorrect and market outcomes may be materially worse than we anticipate. Please see our full disclosure about the limitations of forward-looking statements and the risks of investing at https://quantstreetcapital.com/blog_disclosure/.